2000s energy crisis

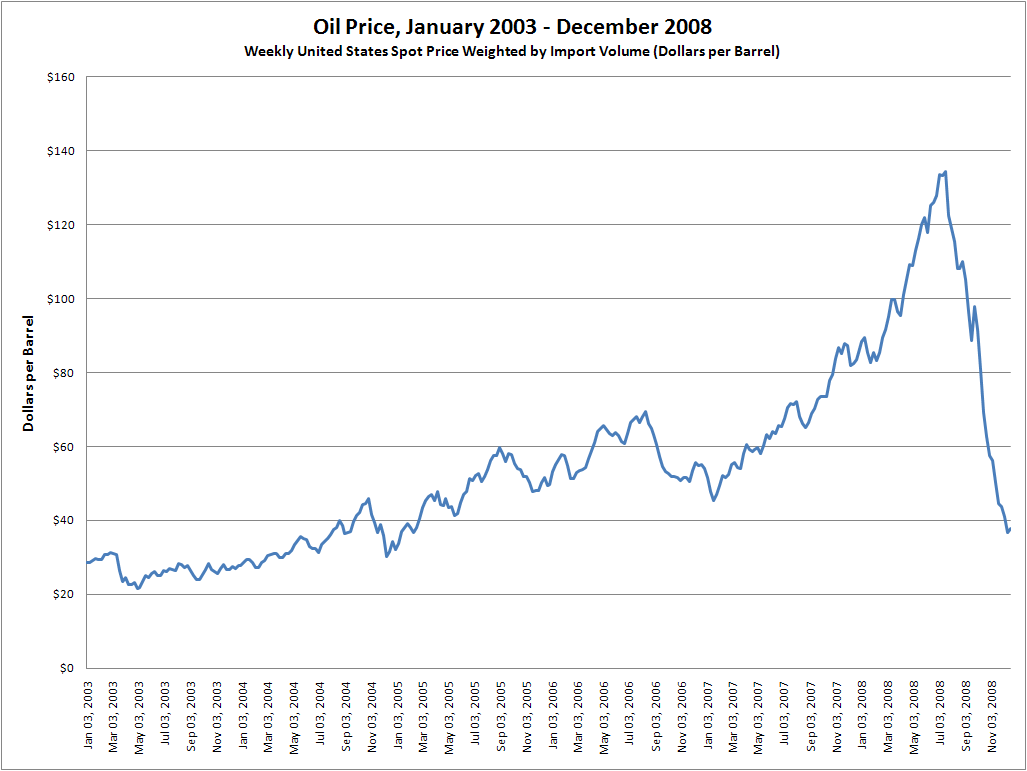

From the mid-1980s to September 2003, the inflation-adjusted price of a barrel of crude oil on NYMEX was generally under US$25/barrel in 2008 dollars. During 2003, the price rose above $30, reached $60 by 11 August 2005, and peaked at $147.30 in July 2008.[1] Commentators attributed these price increases to many factors, including Middle East tension, soaring demand from China,[2] the falling value of the U.S. dollar, reports showing a decline in petroleum reserves,[3][4] worries over peak oil,[5] and financial speculation.[6]

This article is about the causes and analysis of the relatively high oil prices of the 2000s. For a chronology of oil prices during this time, see World oil market chronology from 2003.Date

2003–2008

Third oil crisis

For a time, geopolitical events and natural disasters had strong short-term effects on oil prices, such as North Korean missile tests,[7] the 2006 conflict between Israel and Lebanon,[8] worries over Iranian nuclear plans in 2006,[9] Hurricane Katrina,[10] and various other factors.[11] By 2008, such pressures appeared to have an insignificant impact on oil prices given the onset of the global recession.[12] The recession caused demand for energy to shrink in late 2008, with oil prices collapsing from the July 2008 high of $147 to a December 2008 low of $32.[13] However, it has been disputed that the laws of supply and demand of oil could have been responsible for an almost 80% drop in the oil price within a six-month period.[14] Oil prices stabilized by August 2009 and generally remained in a broad trading range between $70 and $120 through November 2014,[15] before returning to 2003 pre-crisis levels by early 2016, as US production increased dramatically. The United States went on to become the largest oil producer by 2018.[16]

New inflation-adjusted peaks[edit]

The price of crude oil in 2003 traded in a range between $20–$30/bbl.[17] Between 2003 and July 2008, prices steadily rose, reaching $100/bbl in late 2007, coming close to the previous inflation-adjusted peak set in 1980.[18] A steep rise in the price of oil in 2008 – also mirrored by other commodities – culminated in an all-time high of $147.27 during trading on 11 July 2008,[19] more than a third above the previous inflation-adjusted high.

High oil prices and economic weakness contributed to a demand contraction in 2007–2008. In the United States, gasoline consumption declined by 0.4% in 2007,[20] then fell by 0.5% in the first two months of 2008 alone.[21] Record-setting oil prices in the first half of 2008 and economic weakness in the second half of the year prompted a 1.2 Mbbl (190,000 m3)/day contraction in US consumption of petroleum products, representing 5.8% of total US consumption, the largest annual decline since 1980 at the climax of the 1979 energy crisis.[22]

There is debate over what the effects of the 2000s energy crisis will be over the long term. Some speculated that an oil-price spike could create a recession comparable to those that followed the 1973 and 1979 energy crises or a potentially worse situation such as a global oil crash. Increased petroleum prices are reflected in a vast number of products derived from petroleum, as well as those transported using petroleum fuels.[61]

Political scientist George Friedman has postulated that if high prices for oil and food persist, they will define the fourth distinct geopolitical regime since the end of World War II, the previous three being the Cold War, the 1989–2001 period in which economic globalization was primary, and the post-9/11 "war on terror".[62]

In addition to high oil prices, from year 2000 volatility in the price of oil has increased notably and this volatility has been suggested to be a factor in the financial crisis which began in 2008.[63]

The perceived increase in oil price differs internationally according to currency market fluctuations and the purchasing power of currencies. For example, excluding changes in relative purchasing power of various currencies, from 1 January 2002 to 1 January 2008:[64]

On average, oil prices roughly quadrupled for these areas, triggering widespread protest activities.[65] A similar price surge for petroleum-based fertilizers contributed to the 2007–08 world food price crisis and further unrest.[66]

In 2008, a report by Cambridge Energy Research Associates stated that 2007 had been the year of peak gasoline usage in the United States, and that record energy prices would cause an "enduring shift" in energy consumption practices.[67] According to the report, in April gas consumption had been lower than a year before for the sixth straight month, suggesting 2008 would be the first year U.S. gasoline usage declined in 17 years. The total miles driven in the U.S. began declining in 2006.[68]

In the United States, oil prices contributed to inflation averaging 3.3% in 2005–2006, significantly above the average of 2.5% in the preceding 10-year period.[69] As a result, during this period the Federal Reserve steadily raised interest rates to curb inflation.

High oil prices typically affect less-affluent countries first, particularly the developing world with less discretionary income. There are fewer vehicles per capita, and oil is often used for electricity generation as well as private transport. The World Bank has looked more deeply at the effect of oil prices in the developing countries. One analysis found that in South Africa a 125 percent increase in the price of crude oil and refined petroleum reduces employment and GDP by approximately 2 percent, and reduces household consumption by approximately 7 percent, affecting mainly the poor.[70]

OPEC's annual oil export revenue surged to a new record in 2008, estimated around US$800 billion.[71]

Forecasted prices and trends[edit]

According to informed observers, OPEC, meeting in early December 2007, seemed to desire a high but stable price that would deliver substantial needed income to the oil-producing states, but avoid prices so high that they would negatively impact the economies of the oil-consuming nations. A range of US$70–80 per barrel was suggested by some analysts to be OPEC's goal.[72]

In November 2008, as prices fell below $60 a barrel, the IEA warned that falling prices could lead to both a lack of investment in new sources of oil and a fall in production of more-expensive unconventional reserves such as the oil sands of Canada. The IEA's chief economist warned, "Oil supplies in the future will come more and more from smaller and more-difficult fields," meaning that future production requires more investment every year. A lack of new investment in such projects, which had already been observed, could eventually cause new and more-severe supply issues than had been experienced in the early 2000s according to the IEA. Because the sharpest production declines had been seen in developed countries, the IEA warned that the greatest growth in production was expected to come from smaller projects in OPEC states, raising their world production share from 44% in 2008 to a projected 51% in 2030. The IEA also pointed out that demand from the developed world may have also peaked, so that future demand growth was likely to come from developing nations such as China, contributing 43%, and India and the Middle East, each about 20%.[73]

End of the crisis[edit]

By the beginning of September 2008, prices had fallen to $110. OPEC Secretary General El-Badri said that the organization intended to cut output by about 500,000 barrels (79,000 m3) a day, which he saw as correcting a "huge oversupply" due to declining economies and a stronger U.S. dollar.[74] On 10 September, the International Energy Agency (IEA) lowered its 2009 demand forecast by 140,000 barrels (22,000 m3) to 87.6 million barrels (13,930,000 m3) a day.[74]

As many countries throughout the world entered an economic recession in the third quarter of 2008 and the global banking system came under severe strain, oil prices continued to slide. In November and December, global demand growth fell, and U.S. oil demand fell an estimated 10% overall from early October to early November 2008 (accompanying a significant drop in auto sales).[75]

In their December meeting, OPEC members agreed to reduce their production by 2.2 million barrels (350,000 m3) per day, and said their resolution to reduce production in October had an 85% compliance rate.[76]

Petroleum prices fell below $35 in February 2009, but by May 2009 had risen back to mid-November 2008 levels around $55. The global economic downturn left oil-storage facilities with more oil than in any year since 1990, when Iraq's invasion of Kuwait upset the market.[77]

In early 2011, crude oil rebounded above US$100/bbl due to the Arab Spring protests in the Middle East and North Africa, including the 2011 Egyptian revolution, the 2011 Libyan civil war, and steadily tightening international sanctions against Iran.[78] The oil price fluctuated around $100 through early 2014.

By 2014–2015, the world oil market was again steadily oversupplied, led by an unexpected near-doubling in U.S. oil production from 2008 levels due to substantial improvements in shale "fracking" technology.[79][80] By January 2016, the OPEC Reference Basket fell to US$22.48/bbl – less than one-sixth of its record from July 2008 ($140.73), and back below the April 2003 starting point ($23.27) of its historic run-up.[81] OPEC production was poised to rise further with the lifting of Iranian sanctions, at a time when markets already appeared to be oversupplied by at least 2 million barrels per day.[82]